Is Tesco stock a buy for passive income today? Here’s what the charts say

Tesco (LSE: TSCO) stock remains popular with many investors in the UK today. At first glance, that may seem surprising, given that the share price has delivered a 6% loss over 20 years.

This leads me to believe that many investors probably value the dividends on offer from Tesco shares. So, how does the FTSE 100 stock look from a passive income perspective? Here’s what the charts say.

Dividend yield

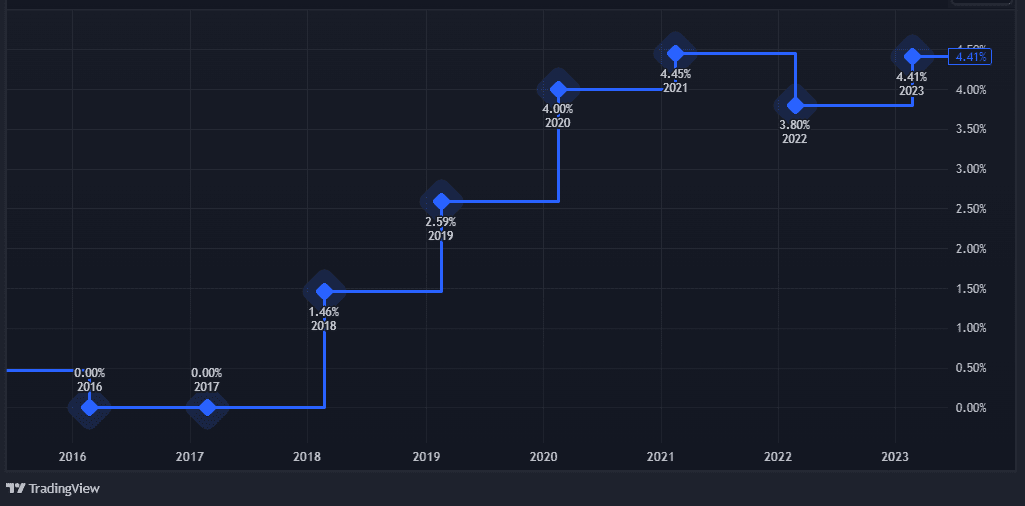

The first thing many investors look at when assessing a dividend stock is the yield. In the case of Tesco, it is currently 4.4%, which is higher than the Footsie average of 3.9%.

In the chart below, we can see that the dividend yield has been trending higher since 2018. This was the year that the supermarket giant reinstated its payout after a 2014 accounting scandal knocked it for six. Hence the 0% yield for 2016 and 2017.

That yield doesn’t look as appealing now that interest rates have risen sharply. I mean, I can lock my cash away in a fixed-term savings account today and get between 5% and 6%.

Of course, by doing this, I forgo passive income while my money is locked away. But the eventual return is arguably more attractive as I don’t have to worry about a falling share price or dividend cuts.

On the flip side, I’d be giving up the chance of potential share price gains on top of rising passive income.

Dividend cover

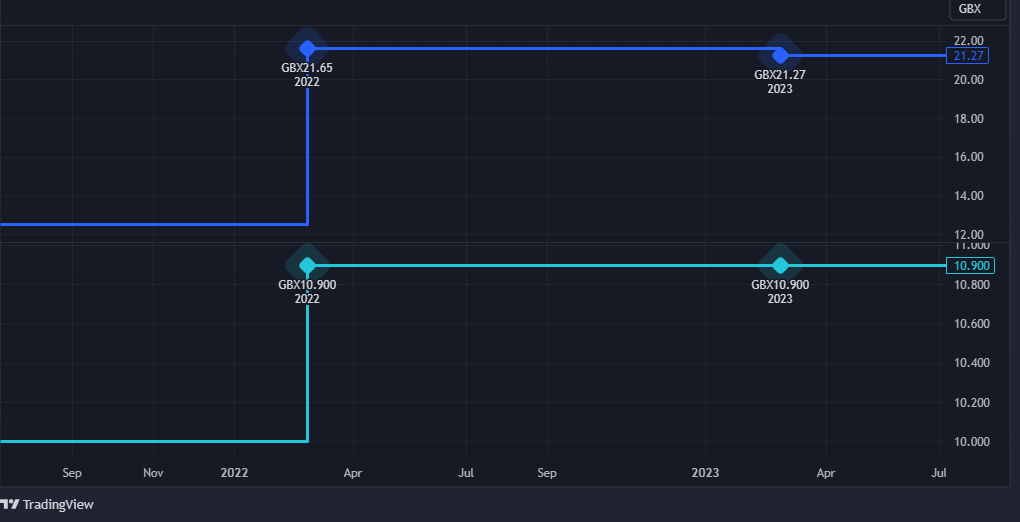

Dividend cover is a popular measure of safety used by income investors. It is calculated by taking the earnings per share (EPS) figure and dividing it by the dividend per share (DPS). Essentially, this metric provides a quick snapshot of how many times the dividend is ‘covered’ by earnings.

The general consensus is that anything around two times or above is considered good coverage.

Above, we can see that Tesco’s dividend is reassuringly covered almost two times by earnings. That is, the EPS figure at the top is that much higher than the DPS figure at the bottom. This means that for every £1 the supermarket pays out, it has another £1 spare (almost) to cover the dividend payment.

Margin compression

Supermarket margins are generally between 1% and 3%. That may not sound like much, but the huge volume of items that Tesco sells means it often adds up to a lot.

However, the company has experienced margin pressure recently. This has been caused by rising input costs from high inflation and fierce industry competition from discounters such as Lidl and Aldi.

Admirably, Tesco has chosen to absorb some of this inflationary pressure rather than passing it all through to cash-strapped customers. But this has compressed its operating margin to 2.3%, down from 4% in 2019.

Would I buy the shares?

The Tesco dividend yield of 4.4% doesn’t sway me to invest in the shares. I can hope to secure double that elsewhere in the FTSE 100 right now.

Meanwhile, industry competition means margins are likely to stay under pressure, resulting in modest dividend hikes. And I don’t see any catalysts on the horizon for long-term share price appreciation.

Putting all this together then, I think there are better passive income options today.

The post Is Tesco stock a buy for passive income today? Here’s what the charts say appeared first on The Motley Fool UK.

Don’t miss this top growth pick for the ‘cost of living crisis’

While the media raves about Google and Amazon, this lesser-known stock has quietly grown 880% – with a:

- Greater than 20X increase in margins

- Nearly 60% compounded revenue growth over 5 years – more than Apple, Amazon and Google!

- A 3,000% earnings explosion

Of course, past performance is no guarantee of future results. However, we think it’s stronger now than ever before. Amazingly, you may never have heard of this company.

Yet there’s a 1-in-3 chance you’ve used one of its 250 brands. Many are household names with millions of monthly website visitors, and that often help consumers compare items, shop around and save.

Now, as the ‘cost of living crisis’ bites, we believe its influence could soar. And that might bring imminent new gains to investors who’re in position today. So please, don’t leave without your FREE report, ‘One Top Growth Stock from The Motley Fool’.

Claim your FREE copy now

setButtonColorDefaults(“#5FA85D”, ‘background’, ‘#5FA85D’);

setButtonColorDefaults(“#43A24A”, ‘border-color’, ‘#43A24A’);

setButtonColorDefaults(“#fff”, ‘color’, ‘#FFFFFF’);

})()

More reading

- Buying 10,810 cheap Tesco shares would give me dividend income of £1,200 this year

- 2 FTSE 100 value shares I’d buy, and 1 I’d avoid!

- How much could £1,000 in Tesco shares be worth in 3 years?

- Is this 4% dividend-yielding stock ideal for passive income?

Ben McPoland has no position in any of the shares mentioned. The Motley Fool UK has recommended Tesco Plc. Views expressed on the companies mentioned in this article are those of the writer and therefore may differ from the official recommendations we make in our subscription services such as Share Advisor, Hidden Winners and Pro. Here at The Motley Fool we believe that considering a diverse range of insights makes us better investors.